The UK’s Plan 2 student loan system has entered a surprising new phase in 2026. Instead of costing the government money, it’s now projected to generate a financial surplus—raising major questions for graduates about fairness, repayments, and whether the system still works in their favor.

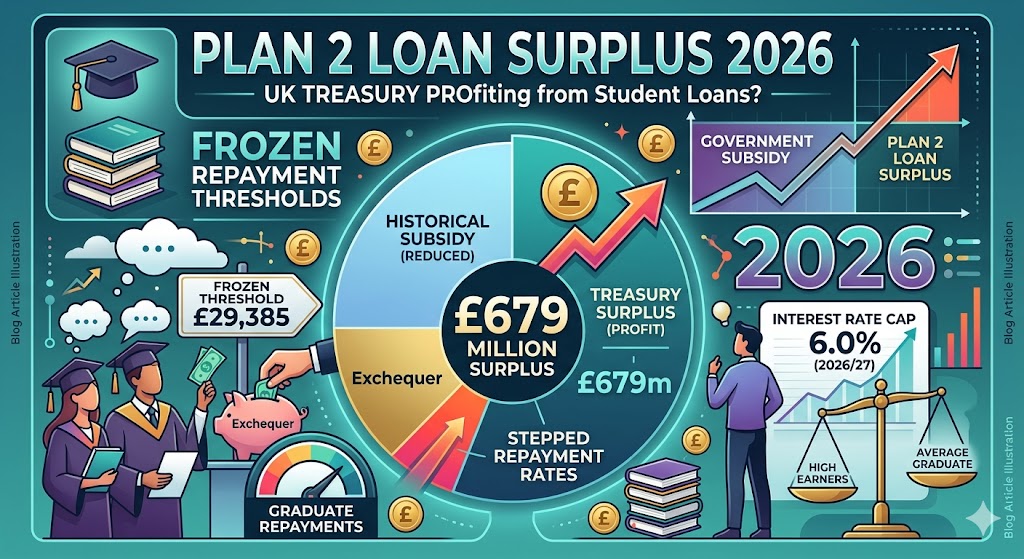

A recent report from the Higher Education Policy Institute highlights that the UK government could earn around £679 million from the final Plan 2 cohort. This marks a major shift—from subsidizing students to effectively profiting from their repayments.

Here’s what’s driving this change and what it means for your finances.

Why Is There a Plan 2 Loan Surplus in 2026?

Originally, student loans were designed with the expectation that many graduates would never fully repay their debt. Any remaining balance would be written off after 30 years, meaning the government absorbed the loss.

That assumption has changed due to three key factors:

1. Frozen Repayment Thresholds

The repayment threshold has been fixed at £29,385 until 2030. As wages slowly rise, more graduates are pulled into repayment—and those already paying contribute more over time.

2. High Interest Rates

Plan 2 loans carry interest rates of up to RPI + 3%, causing balances to grow quickly. Even with caps, many borrowers remain in repayment longer, increasing total contributions.

3. Shift to “Cost-Neutral” Lending

The combination of higher repayments and long repayment periods means the government—via the HM Treasury—is now expected to break even or profit on certain cohorts.

2026 Interest Rate Cap: Helpful or Misleading?

In April 2026, the government introduced a temporary 6% interest cap for Plan 2 and postgraduate loans.

Key Figures for 2026/27:

- Max Interest Rate: 6.0%

- Repayment Threshold: £29,385 (still frozen)

- Repayment Rate: 9% above the threshold

- Loan Write-off: After 30 years

What It Really Means

While the cap sounds positive, it mainly benefits high earners who are likely to repay their loans in full.

For most graduates, the real financial pressure comes from the frozen threshold, which effectively increases monthly repayments and reduces take-home pay.

Calls for Reform: The Stepped Repayment Proposal

With the system now generating surplus revenue, pressure is growing for reform.

Both the National Union of Students and HEPI are advocating for a stepped repayment model, where contributions scale with income:

- 3% on lower income bands

- 5% on mid-level earnings

- 7% on higher earnings

This approach would make repayments more progressive and reduce the burden on middle-income graduates.

Should You Overpay Your Student Loan in 2026?

This is one of the most important financial decisions graduates face.

The Reality:

For most borrowers, overpaying is not worth it.

If you’re unlikely to fully repay your loan within 30 years, any extra payments you make now won’t benefit you—they simply reduce the amount eventually written off.

When Overpaying Might Make Sense:

- You earn £60,000+ consistently

- You’re on track to fully repay before the write-off period

- You want to reduce total interest paid

Otherwise, Plan 2 loans function more like a graduate tax than a traditional debt.

What This Means for Graduates in 2026

The emergence of a student loan surplus signals a major shift in UK education finance. What was once a government-supported system is now generating revenue—raising concerns about fairness and long-term sustainability.

As discussions continue, including scrutiny from the Treasury Committee, graduates should:

- Monitor their payslips closely

- Stay updated on policy changes

- Think carefully before making extra repayments

Final Thoughts

The Plan 2 loan surplus in 2026 highlights a system that has quietly transformed. While some benefit, many graduates are paying more for longer—without clear advantages.

Understanding how these changes affect your income and long-term finances is essential in navigating the evolving landscape of student loans in the UK.