Ontario students preparing for the 2026–2027 school year are facing major changes to OSAP funding. While many headlines are calling it an “OSAP increase,” the reality is more complicated.

Yes, students may still qualify for similar funding amounts — but a much larger portion of that money will now come as repayable student loans instead of grants.

For thousands of students across Ontario, this could mean graduating with significantly more debt than previous years.

If you’re applying for OSAP in 2026, here’s a complete breakdown of the new rules, tuition changes, grant reductions, and ways to reduce your student debt.

What Is Changing With OSAP in 2026?

Starting on August 1, 2026, Ontario is introducing a new OSAP funding structure that changes how student aid is distributed.

The biggest update is the shift from grants to loans.

In previous years, many students received most of their financial aid as non-repayable grants. Under the new system, provincial grants will be limited, while loans will make up the majority of funding packages.

This change affects students attending:

- Ontario universities

- Public colleges

- Private career colleges

- Professional and certificate programs

The goal, according to the province, is to create a more sustainable long-term student aid system. However, many students are worried about the increase in post-graduation debt.

The Biggest OSAP Change: More Loans, Fewer Grants

How OSAP Worked Before

Before the 2026 changes, eligible students could receive up to:

- 85% of their funding as grants

- Only a smaller percentage as loans

This helped reduce long-term student debt and made higher education more affordable for low-income families.

How OSAP Will Work in 2026

Beginning in the 2026–2027 academic year:

- Provincial grants are capped at 25%

- The remaining 75% will be issued as loans

That means students may still receive similar total funding amounts, but much more of that money must eventually be repaid.

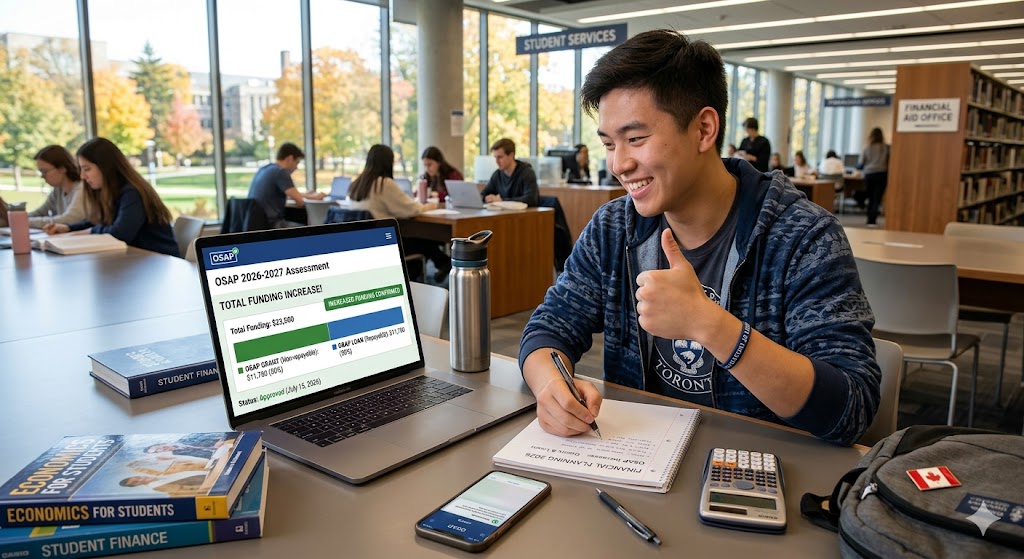

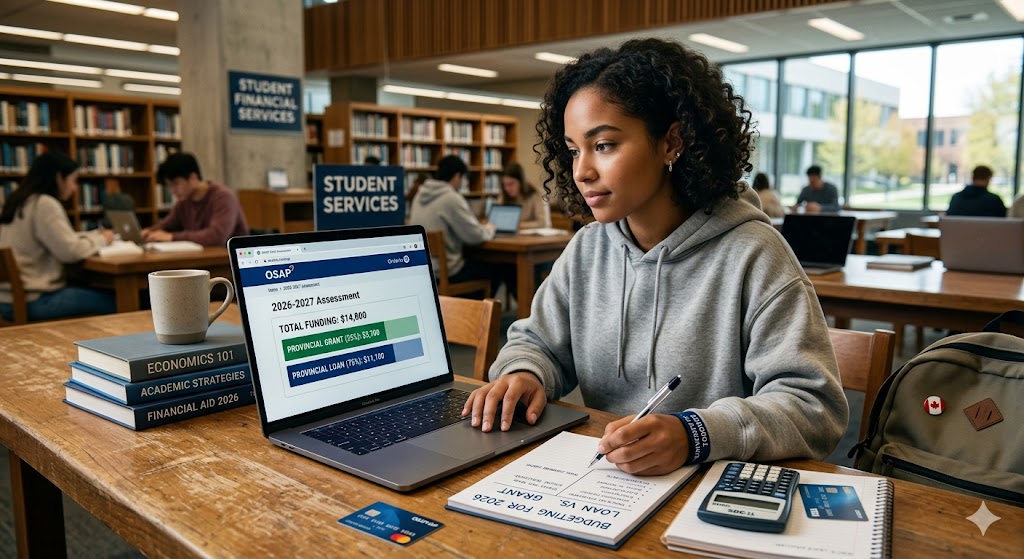

Example of the New OSAP Loan Structure

Here’s a simple example:

Before 2026:

A student receiving $12,000 in OSAP might get:

- $10,000 in grants

- $2,000 in loans

Starting in 2026:

That same student could receive:

- $3,000 in grants

- $9,000 in loans

That’s roughly $6,000–$8,000 more debt every year for the average Ontario student.

Over a four-year degree, that could add up to tens of thousands of dollars in additional student loan debt.

Private Career College Students Will Be Hit Hardest

Students attending private career colleges are facing even tougher changes.

Beginning in 2026:

- Provincial grants for private career colleges are being eliminated

- All provincial aid will be provided entirely through loans

This means students in private institutions may no longer receive any provincial grant funding at all.

If you’re considering a private college program, it’s important to carefully calculate your future debt before enrolling.

Ontario Tuition Freeze Is Officially Ending

Another major change happening alongside OSAP reform is the end of Ontario’s tuition freeze.

After seven years of frozen tuition rates, publicly funded colleges and universities can now increase tuition by:

- Up to 2% per year

- For the next three years

While a 2% increase may not sound huge, combined with the new OSAP loan-heavy structure, students will likely need to borrow even more money to cover education costs.

Will Students Still Receive Enough OSAP Money?

In most cases, yes.

The province says overall funding limits and weekly maximums are expected to remain stable or slightly increase to reflect rising tuition and living expenses.

However, the major difference is this:

Students will now borrow more of that funding instead of receiving it as grants.

So while your upfront school costs may still be covered, your repayment burden after graduation could become much larger.

Is the Federal Portion of OSAP Changing?

No.

The new changes mainly affect the Ontario provincial portion of OSAP.

The federal government’s Canada Student Grants are calculated separately and are not included under Ontario’s new 25% grant cap.

This means students may still receive some non-repayable federal assistance depending on eligibility.

Does OSAP Still Stay Interest-Free While You’re in School?

Yes.

OSAP loans remain interest-free while you are enrolled as a full-time student and maintaining eligible status.

Interest only starts accumulating after:

- You graduate

- You leave school

- Your six-month grace period ends

This gives students some breathing room before repayment begins.

Financial Aid Programs That Can Still Help Students

Even with these changes, there are still several ways to reduce your overall student debt.

1. Student Access Guarantee (SAG)

The Student Access Guarantee helps students whose OSAP funding does not fully cover essential education costs.

If OSAP falls short for expenses like:

- Tuition

- Textbooks

- Mandatory fees

your college or university may provide additional bursaries or emergency financial aid.

Students should contact their school’s financial aid office directly to learn what support is available.

2. Scholarships and Bursaries

With grants shrinking, scholarships are becoming more important than ever.

Students should start searching early and apply aggressively for:

- Entrance scholarships

- Merit-based awards

- Community bursaries

- Need-based financial aid

Many Ontario schools are expected to introduce new financial aid programs in 2026 to help offset the OSAP changes.

3. Ontario Learn and Stay Grant

The Learn and Stay Grant remains one of the best funding opportunities available in Ontario.

Eligible students in high-demand healthcare programs such as:

- Nursing

- Paramedicine

- Medical laboratory sciences

may receive full grant funding if they agree to work in underserved Ontario communities after graduation.

For qualifying students, this can dramatically reduce student debt.

How to Reduce Your OSAP Debt in 2026

With student loans increasing, financial planning is becoming more important for Ontario students.

Here are smart ways to reduce future debt:

Live at Home if Possible

Housing is often the largest expense for students.

Apply for Scholarships Early

Treat scholarship applications like a part-time job.

Work Part-Time

Even a small income during school can reduce borrowing needs.

Create a Monthly Budget

Tracking expenses can help avoid unnecessary debt.

Consider Declining the Loan Portion

One of the most overlooked OSAP features is that students can choose to:

- Accept grants

- Decline loans

If you have savings, family support, or part-time income, this can help you graduate debt-free.

How to Estimate Your 2026 OSAP Funding

Ontario updates the OSAP Aid Estimator every spring.

Students should use the official estimator as soon as the 2026–2027 version becomes available to see:

- Estimated grants

- Estimated loans

- Tuition coverage

- Expected repayment amounts

This is the best way to understand how the new grant-to-loan ratio will affect your personal finances.

Student Concerns About the 2026 OSAP Changes

Many Ontario students and student advocacy groups have raised concerns about the new funding model.

Common concerns include:

- Rising student debt

- Reduced affordability

- Financial stress after graduation

- Accessibility barriers for low-income students

Some student organizations are also pushing for:

- Lower interest rates

- Expanded grants

- Longer repayment grace periods

- More institutional bursaries

As the 2026 school year approaches, discussions around student affordability are expected to continue growing.

Final Thoughts

The 2026 OSAP changes represent one of the biggest shifts in Ontario student funding in years.

While students may still receive enough aid to cover school costs, the reality is clear:

Much more of that aid will now come in the form of repayable loans instead of grants.

For many students, this means:

- Higher debt after graduation

- Greater reliance on budgeting and financial planning

- Increased importance of scholarships and bursaries

- More pressure to manage education costs carefully

If you’re planning to attend college or university in Ontario in 2026, the best thing you can do is prepare early, understand your funding options, and build a strategy to minimize unnecessary borrowing.

Smart planning today could save you thousands of dollars in student debt tomorrow.